"jcr:9c764063-c2e8-4ac4-910b-fd8821a39db5" (String)

Choose your language

Rural & Smart Agri-finance Development

Lower risks and costs for financial institutions servicing the Agriculture and Agri-food Sectors

Our advisory services are guided by a holistic approach to sustainable rural and smart agri-finance development. This approach combines access to finance for farms of all sizes, agribusinesses, rural enterprises, and households with improved technological solutions and cost-efficient delivery channels.

To maintain a healthy loan portfolio, agricultural lending requires special expertise and tools to better evaluate the activity of farmers and agri-food enterprises. As a result, we help financial institutions to develop innovative technologies, tools, and financial products that reduce both risks and costs, and which can be used to overcome traditional barriers of financial service provision to the agriculture and agri-food sectors.

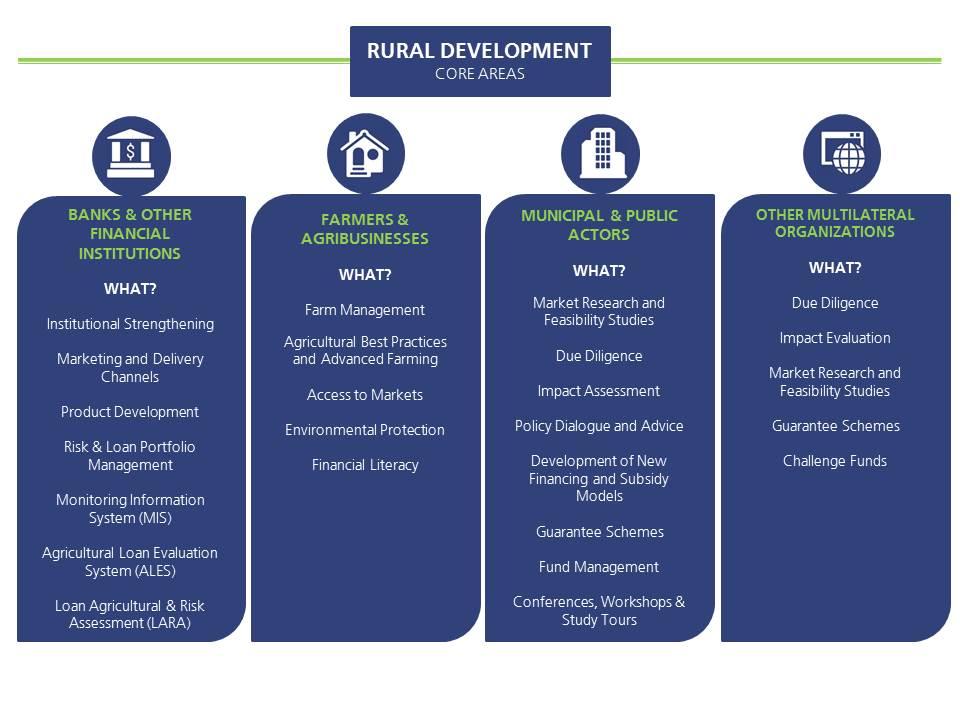

We offer advisory services to four main target groups:

Training services

The provision of training courses across a large range of topics is another crucial part of our services. Classroom and digital workshops, as well as on-the-job training and coaching sessions are the most important training methods we use.

We also offer the following microfinance topics within our Development Finance Academies:

- Certified Expert in Agricultural Finance;

- Certified Expert in Sustainable Finance;

- Certified Expert in Climate Adaptation Finance.

The Frankfurt School Development Finance e-Campus has become a very successful e-learning tool for professionals interested in Rural & Smart Agri-finance Development.

Flagship Projects

Europe l EIB l 2019 – 2020

Turkey, Caucasus & Central Asia l EBRD l 2017 – 2020

Mapping Agribusiness Support Measures in Turkey (Phase II & III)

LatAm & Caribbean l IDB Invest l 2018 – 2020

Turkey, Caucasus & Central Asia l AFD l 2018 - 2023

Core Services

Banks and other financial institutions (FIs)

To maintain a healthy loan portfolio, agricultural lending requires special expertise and tools to better evaluate the activity of farmers, as well as food and beverage manufacturers. To achieve this, we help FIs develop innovative technologies, tools, and financial products that lower both risks and costs. We offer the following advisory services to financial institutions:

Market, Production and Climate Risks

We work with agronomists who provide concrete advice about agriculture to create a risk management structure. Using climate maps, they identify climate risks that can be mitigated with loans.

Credit, Operation and Liquidity Risks

Risk in agricultural lending differs from other types of lending because of the sector’s seasonality and other externalities. We have established tools and technologies that support FIs to manage credit, operational and liquidity risk in agricultural lending. Our advice enables FIs to align practices with existing domestic risk regulations. We foster the creation of comprehensive risk management structures with a clear set of policies and pragmatic guidelines to manage agricultural businesses.

Loan Portfolio Management

The management of risk in agricultural lending is based on the quality of client data. IAS helps establish procedures to manage and control risks. Our loan portfolio management services start with an assessment of current portfolio reports and the use of our Monitoring Information System (MIS). This is followed by an evaluation of current reporting of key indicators in agriculture such as crop, region, maturity, etc. This portfolio classification helps the institution to better identify risks and to make the right decisions.

Monitoring Information System (MIS)

A well-structured MIS is an important tool to manage loan portfolios. However, to function properly, detailed information is required and must be provided by the risk department. We help our clients select the parameters that will feed into the data base. IAS works together with the IT department, which at a later point will prepare the reports for the credits department and management.

Agricultural Loan Evaluation System (ALES)

One of the major impediments to agricultural lending is the high cost of evaluating borrower creditworthiness. The specific nature and diversity of agricultural activities requires sophisticated agronomic know-how. However, it is expensive to use “expert” loan officers to collect and evaluate borrowers and anticipate cash flows. As a result, many agricultural micro, small and medium enterprises (MSMEs) and households remain without access to finance. However, increasing demand for agricultural commodities, as well as rising competition in urban areas, has led financial institutions (FIs) to re-examine this market segment. FIs in this space demand innovative approaches to implement agricultural loan products with risk evaluation systems that calculate cash flows and thus reduce costs.

In response to these challenges, IAS has developed an innovative scoring tool called ALES.

Loan Agricultural & Risk Assessment (LARA)

Often, FIs do not have tools to analyse agricultural loans and risk. To cope with this problem, we have developed LARA, which helps loan officers and decision-makers to better understand agricultural loans. LARA enables the analysis of market, production, moral hazard, and climate change risks on the basis of an individual cash flow that integrates all of the farmer’s income and expenses.

Institutional Strengthening

Developing of Policies and Procedures for FIs

The development or adjustment of procedures to implement and manage agricultural loans is crucial. We account for local specificities that effect these products, such as the FI’s risk appetite, the competitive positioning in the country’s agricultural and rural lending market, and future targets.

We design policies and procedures for FIs involved in rural and agricultural lending, enabling them to:

- achieve efficiency;

- implement appropriate risk management;

- reduce costs;

- respond quickly to client demands;

- adapt products to real needs.

Organizational Structure

A well-structured agricultural finance unit guarantees the optimization of operations and adequate control of risks. We support FIs in establishing organizational structures dedicated to agriculture by defining responsibilities towards managing potential risks rising from operations and training the staff.

Training, Coaching, Training of Trainers (ToT)

To build internal capacities, we offer technical assistance in the form of trainings (classroom lectures, seminars or workshops), on-the-job training, and coaching. In order to sustain rural lending over time and foster growth, we establish "multiplier" mechanisms that institutionalise and ensure capacity-building. Building upon its extensive experience and training programmes worldwide, IAS offers an integrated approach: designing and implementing comprehensive capacity building processes that focus on both the branch and regional/head office levels.

We offer a Training of Trainers programme to enable ongoing training activities and ensure the knowledge transfer extends beyond the scope of the assignment. It provides internal trainers with skills to teach training development, material development, and adult learning.

HR Support

Rural and agricultural lending is distinctive from other lending activities. IAS helps FIs review their network structure and staff capacity, and to make necessary changes in organisational and qualification requirements. Moreover, we provide tailored trainings to staff and help our clients in hiring new staff for agricultural and rural banking services. We employ agronomists as relationship managers who communicate with rural communities, identify their needs, and provide further guidance if necessary. This enables FIs to bundle financial and non-financial products/services and offer packages for agricultural producers. With this HR strategy, we improve the competitive positioning of the institution in the market, and help to monitor lending risks.

Product Development, including value chain finance, warehouse receipts, working capital and investment loans

Loan Products

Product design is an essential element in the optimisation of operations for FIs. Therefore, we offer a full range of services that includes market and institutional assessment, product design and definition, product adjustment, value chain identification, pilot test, pilot test assessment, and final roll-out.

Agri-Card

Since the cash flow cycle in agricultural production does not conform to the monthly cycles of credit cards, IAS has developed a special agricultural credit card called the Agri-Card. It allows agricultural producers to purchase agricultural inputs and repay to the bank during harvest time. In addition to operational efficiency, clients can define cash limits for items. This provides a method to control farmers’ expenses and ensure that they only spend for agricultural production.

Warehouse Receipt Finance

Financial instruments, such as warehouse receipts, help institutions reduce the risk of agricultural lending. They also enable farms to access loans while waiting for a better price for their products. In order to work, such schemes must be well developed and legally viable. We support financial institutions that wish to develop this product by identifying strategic partners and establishing links for financial schemes based on warehouse receipts.

Project and Investment Finance

Some FIs focus on the higher end of the rural and agricultural lending market through agricultural investment and project finance. Financing these large investment projects requires agronomic risk analysis and projection skills. For such clients, IAS works with agronomists and agri-lending experts who are specialised in a broad range of farming and agriculture products. IAS provides insight into farm business strategy, operations, production, processing, marketing, product diversity, technology transfer, planning labour and machinery, use of machinery and equipment, benchmarking with comparative performance data, quality control, budget and cash flow preparations, financial projections, and credit management. Our consultants transfer both the technical and business skills required to service these select agricultural enterprises.

Value Chain Finance

Value chains are essential structures in the commercialisation of agricultural products, especially for small farmers. Strengthening links within the value chain ensures that small producers can generate income and repay loans, which translates into better agriculture portfolios and cost reductions for FIs. Our services identify potential agriculture value chains for financing. We can create or adapt financial products to meet the individual characteristics of a value chain. This includes financing schemes, value chain mapping, establishing links between value chain actors, implementing agricultural value chain finance mechanisms, rebuilding and restructuring value chains through innovative financial products, team building to increase the cohesion of actors, and fostering coordination among value chain actors.

Marketing and Delivery Channels

Banking Agents

The high cost of financial services can be reduced by using alternative delivery channels. These channels include banking agents, strategically identified shops, pharmacies, and retailers who increase accessibility to clients. Building such channels increases efficiency and cuts costs for FIs. We support FIs in this space through strategizing, planning and implementing agency banking as a core delivery channel. Our services include:

- the design of a detailed business case;

- market assessment to identify potential businesses that can serve as agents;

- defining the range of services and products to be provided;

- developing marketing materials;

- providing trainings for a successful launching of the services.

Mobile Banking

Mobile banking is a high-outreach delivery channel that allows rural and urban populations easy access to financial products and services. This delivery channel is cost efficient for FIs and easy for end-clients to use. We provide services that help FIs define and implement mobile banking strategies. Our services cover: organisational alignment and capacity building; technology/system requirements identification; risk assessment and internal control definition; product development; marketing and customer education; regulatory compliance; and the introduction of mobile channels.

Marketing for Agricultural Loans

Agricultural products need marketing strategies that take into consideration the characteristics, idiosyncrasies, and environments of rural clients. We help our clients develop a marketing strategy and create appropriate materials. Furthermore, high transaction costs plague both FIs and clients in rural areas. Therefore, as part of a marketing strategy, we help FIs find and establish delivery mechanisms that reduce risk. We also investigate the applicability, required investment, potential risks, and benefits together with the FI management team.

2. Farmers and Agri-food Enterprises

Often, small and medium-sized farmers, as well as small agribusinesses lack knowledge or access to technical solutions to commercialise their produce and achieve higher turnover. As a result, it is important to not only promote access to finance but also to provide technical support, either directly or through strategic alliances with service providers. On a larger scale, this will help foster the development of an efficient and market-oriented agricultural industry. We provide a number of services to support from-farm-to-fork development and promote sustainable farming.

Farm Management

An optimal farm management structure means a better use of resources and practices in daily agricultural activities. Farm management enhancement increases agricultural yields and production. We support farmers and agri-business in financial management, project design and planning for new investments, process optimisation, quality improvement, and the introduction of new technology.

Farming Techniques and Equipment

To improve the commercial viability of farmers and boost productivity, innovative technologies and practices are of central importance. We support farmers to utilise these opportunities to increase yields, efficiently manage inputs or adopt new crops and production systems.

We also provide advice to farmers that want to upgrade equipment or replace old machinery that has exceeded its lifespan. We also support equipment providers in strengthening their operations and identifying new clients.

Agricultural Best Practices and Advanced Farming

The introduction of best practices and advanced farming methods will increase yields and the quality of agricultural products, while at the same time make them sustainable. For this reason, we teach farmers and agricultural SMEs about crop rotation, use of inputs, correct planting, crop monitoring, harvesting, livestock management, feeding, and the use of medicines and machinery.

Access to Markets

Enabling farmers and agricultural SMEs to access markets with competitive prices is fundamental to a strong agricultural sector and the income of rural households. We advise farmers and SMEs on the identification of value chain schemes, contract farming, and warehouse schemes. This helps them to complete the full cycle from production to end sale.

Environmental Protection and Circular Economy

The sustainable development of farms and agricultural SMEs helps minimise environmental impact, which is a key objective in the age of climate change. We work together with agriculture stakeholders on responsible agricultural practices, conservation, energy efficiency and renewable energy generation, and the adoption of climate change adaption measures.

Climate Smart Agriculture

We are supporting farmers and governments to build resilience to climate change and adapt farming systems that ensure food security while simultaneously conserving natural resources. Another cornerstone of our work is capacity building to help farmers adapt their practices.

Remote Sensing Technology

Remote Sensing can provide numerous insights to financial institutions such as acreage estimation or information on the condition of agricultural crops. Remote sensing can replace costly monitoring visits. We are advising financial institutions interested in using this technology.

3. Municipal, Public and Other Multilateral Actors

We also realise the benefits of working at a macro level in the agricultural sector, for example to develop or improve programmes intended for farmers and financial institutions. Therefore, we offer policy advice and other services to ministries, second-tier banks, and other bilateral and multilateral organizations (e.g. AFD, EBRD, EC, KfW, etc.) to support the development of a more competitive agriculture and agri-food sector by offering:

Market Research and Feasibility Studies

We carry out research and data analysis to identify market opportunities for financing agriculture projects, as well as projects in other sectors of rural areas. Our feasibility studies help structure and implement credit lines, as well as to set-up additional financial products and services.

Due Diligence

Funds and donors need information about partner FIs to understand and optimise their investments. Carrying out due diligences of FIs is part of our core business. After collecting and analysing quantitative and qualitative information, we elaborate reports with recommendations for our clients.

Impact Assessment

We conduct impact assessment studies to measure the direct and indirect impact of the program and the achievement of the indicators. Our impact assessments detail not only achievements, but also challenges, which we address with recommendations and lessons learned.

Policy Dialogue and Advice

Agricultural finance is once again an important issue for governments and donors. In order to advise stakeholders properly and design the right policies, it is fundamental to understand both the financial and agricultural sectors, as well as to have experience on the ground with civil society. We advise our clients and help them to design and implement policies that strengthen the sector.

Development of New Financing and Subsidy Models

Small farmers often require support in the form of subsidies. However, a good business strategy is much more important for them. Subsidy schemes that farmers actively participate in can substantially improve production. Thus, investments can contribute to the development of the agricultural sector. The IAS develops subsidy models once it understands the structures, needs, and potential of the sector.

Guarantee Schemes

Guarantee schemes have had both positive and negative results. Therefore, it is crucial to develop good concepts, structures, and procedures to implement such schemes. Guarantee schemes, which involve several stakeholders, support the investments of farmers, reduce risk and ensure sustainability for FIs. In our services, IAS takes into consideration all of these aspects and aims to optimise impact.

Fund Management

Some donors see funds with specialized credit lines as a mechanism to reach farmers. Some farmers are aided by technical assistance, which guarantees the development of tools and technology to serve the sector. We help our clients design and implement such structures.

Conferences and Workshops

We have organized many conferences and workshops on rural and agricultural finance at international and national levels. Such events provide a unique platform for knowledge and experience exchange by bringing together the key actors involved in agricultural finance, including key decision makers and government practitioners, the private sector, and leading FIs, as well as regulatory and supervisory bodies. These events are essential to drawing the attention of the regional financial sector to the importance of agricultural finance for sustainable growth, as well as towards new trends in agricultural and rural finance.

Study Tours

Introduction of appropriate incentive mechanisms among FI staff is crucial for adoption of the programme by loan officers and the achievement of satisfactory loan disbursements. Aside from financial incentives that can be developed together with the banks’ HR departments and business segments, non-financial incentives have also proven to be important. For that purpose, we organise study tours for loan officers/relationship managers to see in person best practices in agricultural and rural banking. Participants also have the opportunity to visit high-tech agricultural facilities in their region.

.jpg)

Contact

Katia Goertz

Director

Erdal Kocoglu

Director, Turkey Regional Office